How to Learn Savings: A Masterclass in Financial Foundation for 2026

The traditional concept of a rainy day fund is officially obsolete in an economy defined by persistent inflation and rapid technological disruption. You likely feel the pressure of eroding purchasing power while navigating a fragmented landscape of over 25,000 global fintech platforms. It's clear that without a rigorous framework, even the most advanced digital tools lead to analysis paralysis rather than actual capital accumulation. This lack of a structured financial curriculum prevents many professionals from achieving the mastery necessary to secure their long-term objectives and future-proof their assets.

This masterclass provides the definitive architectural principles required to learn savings through a lens of behavioral psychology and AI-powered optimization. By applying these sophisticated, data-driven systems, you'll transform erratic cash flow into a repeatable engine for generating investable capital. We will deconstruct the specific methodologies used to master personal liquidity and ensure your financial foundation remains resilient against the market standards of 2026. This is your path to establishing total confidence in your financial decision-making process and gaining absolute control over your economic ecosystem.

Key Takeaways

- Adopt a professional discipline of capital retention by engineering a structured architecture tailored to your specific financial ecosystem.

- Implement AI-driven budgeting tools to evolve from manual oversight to a high-performance system of algorithmic capital allocation.

- Master the psychological principles necessary to learn savings as a foundational skill, ensuring your capital retention grows in tandem with your income.

- Execute a surgical cash flow audit to identify the precise technical indicators that signal when your savings engine is ready to scale into an investment engine.

- Establish a definitive safety net using the "Six-Month Rule" to future-proof your capital against market volatility and unforeseen industry shifts.

Defining the Savings Ecosystem: More Than Just Piggy Banks

To truly learn savings, you must transition from a consumer mindset to a rigorous framework of capital retention. This process is not about the casual accumulation of funds for a vacation or a luxury purchase. Instead, it represents the professional discipline of securing capital to fuel future growth and stability. While saving for a purchase is merely a deferred expense, saving for capital is the foundational act of wealth creation. Professionals in the 2026 economic environment recognize that idle cash is a decaying asset. With global inflation rates projected to impact purchasing power by as much as 3% to 4% annually, the cost of waiting to establish a robust savings protocol is historically high.

Financial literacy serves as the non-negotiable prerequisite for these efforts. Before you can deploy capital into complex market instruments, you must master the mechanics of your own balance sheet. This baseline mastery is often detailed in a comprehensive guide to personal finance, which outlines how structured budgeting and liquidity management form the bedrock of all successful investment portfolios. Without this foundation, any attempt at wealth building remains speculative and high-risk.

The Mathematical Reality of Compound Interest

Compound interest is the eighth wonder of the world for savers. Its power lies in the exponential growth of reinvested earnings, but this power is highly sensitive to time. The cost of delay is the most punitive tax on your future wealth. For instance, an individual who begins their savings journey at age 25 rather than waiting until age 26 can see a difference of over $54,000 in a standard retirement account by age 65, assuming a consistent 7% annual return. Liquidity remains a critical factor in this ecosystem; your capital must be accessible enough to handle immediate requirements while remaining productive enough to outpace inflationary pressures. Balancing these two needs is the hallmark of a sophisticated financial strategy.

Savings as Your First Investment Strategy

Think of every dollar you retain as a soldier in your future investment army. These units are ready to be deployed into assets that generate passive yield. To effectively learn savings, you must first understand finance literacy and how it dictates your overall risk tolerance. Your emergency fund functions as the insurance policy for your entire investment portfolio. It provides a necessary buffer that prevents you from being forced to liquidate high-performing assets during market downturns. By securing three to six months of operating expenses, you ensure that your long-term strategy remains intact regardless of external market volatility or personal financial shocks.

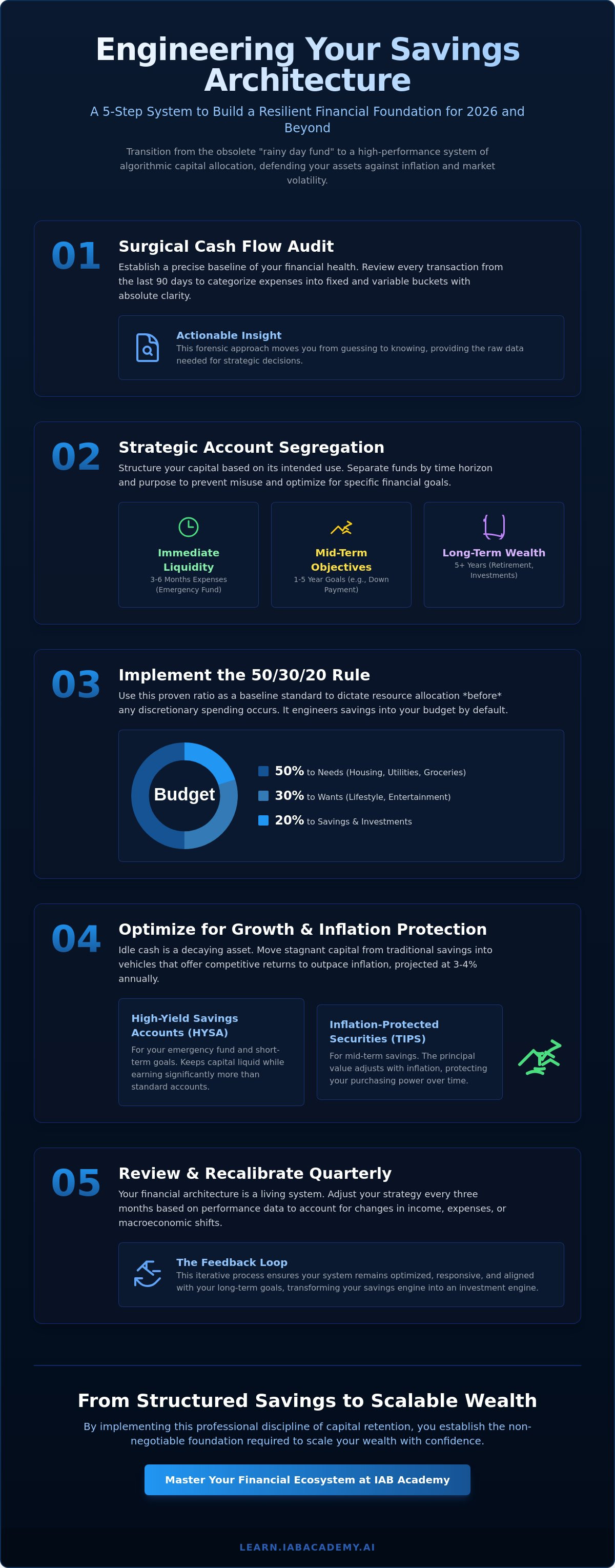

Engineering Your Savings Architecture: A 5-Step System

Establishing a robust financial foundation demands a shift from passive observation to active engineering. To effectively learn savings, you must implement a structured system that prioritizes capital preservation and strategic growth over impulsive consumption. This architecture functions as a defense mechanism against market volatility and inflation.

- Step 1: Audit your existing cash flow with surgical precision. Review every transaction from the last 90 days to establish an accurate baseline of your financial health.

- Step 2: Segregate accounts based on Time Horizon and Purpose. Separate your immediate liquidity from mid-term objectives and long-term wealth preservation.

- Step 3: Implement the 50/30/20 rule as a baseline standard. Use this ratio to dictate your resource allocation before any discretionary spending occurs.

- Step 4: Optimize for high-yield environments and inflation-protected vehicles. Move stagnant cash into assets that offer competitive returns, such as high-yield savings accounts or Treasury Inflation-Protected Securities.

- Step 5: Review and recalibrate based on quarterly performance data. Adjust your strategy every three months to account for changes in income, expenses, or macroeconomic shifts.

Auditing Cash Flow: The Forensic Approach

A forensic audit requires you to categorize expenses into fixed and variable buckets without ambiguity. Fixed expenses include non-negotiable obligations like mortgage payments or insurance premiums. Variable expenses encompass discretionary choices like dining and entertainment. It's vital to identify phantom subscriptions and micro-leaks; recent 2025 consumer reports indicate that the average professional loses $280 annually to forgotten digital services.

Your primary KPI is the Net Savings Rate. This is the percentage of your take-home pay that remains after all expenses are settled. In the 2026 fiscal environment, a Net Savings Rate below 15% is considered high-risk for those seeking long-term stability. Tracking this metric monthly ensures you remain accountable to your growth targets.

The 50/30/20 Rule in a 2026 Economy

The 50/30/20 framework remains the gold standard for balanced wealth management. It allocates 50% of income to Needs, 30% to Wants, and 20% to Savings. If you reside in a high-cost urban environment where rent exceeds 35% of your income, you must aggressively compress the Wants category to protect your savings floor. The objective is to maintain the 20% threshold regardless of external price pressures.

This 20% allocation isn't merely a safety net; it's the capital required for future stock market participation. Without this consistent influx of capital, you cannot leverage compound interest or participate in equity growth. If you want to learn savings at a professional level, you must treat this 20% as a mandatory tax you pay to your future self. Professionals who want to refine their fiscal management can benefit from mastering these foundational standards through structured curriculum paths.

Leveraging AI and Technology for Automated Capital Growth

Transitioning from manual budgeting to algorithmic capital allocation represents the most significant shift in personal finance for 2026. You no longer need to rely on willpower to manage your balance sheet. Predictive AI tools now analyze recurring liabilities and discretionary spending patterns to forecast cash flow shortages before they occur. This technological shift allows users to learn savings through a data-driven lens rather than emotional guesswork. By deploying Smart Instructor™ logic, individuals receive real-time updates that adjust savings targets based on live market volatility and personal consumption habits.

The AI Fintech Ecosystem in 2026

The 2026 fintech landscape is dominated by tools that prioritize predictive accuracy and seamless execution. Leading platforms like Rocket Money, Cleo, and Monarch Money utilize sophisticated machine learning to identify the precise moment to move funds into high-yield accounts without risking liquidity. These algorithms scan for idle cash that isn't required for upcoming liabilities, effectively uncovering hidden savings within your existing bank balance. Integrating these automated processes into your broader financial literacy curriculum ensures that your capital growth remains consistent regardless of market fluctuations. Mastery of these tools is now a prerequisite for professional financial stability.

- Rocket Money AI: Utilizes neural networks to negotiate bills and redirect the difference into index funds automatically.

- Cleo 4.0: Employs generative AI to provide real-time coaching on spending limits based on your 2026 financial goals.

- Monarch Money: Features multi-account synchronization that uses machine learning to optimize tax-advantaged transfers.

The Power of the 'Invisible Save'

Automating the "Pay Yourself First" principle is the most effective way to secure long-term wealth in a high-inflation environment. By implementing direct payroll splits, capital is diverted to savings or investment vehicles before it ever reaches a checking account. This "invisible save" methodology removes human bias and decision fatigue from the equation. Data from behavioral finance reports in early 2026 indicates that removing the human element from saving increases success rates by 80 percent compared to manual transfers. This hands-off approach ensures that your efforts to learn savings are backed by structural discipline.

Round-up rules further enhance this strategy by converting everyday transactions into micro-investments. Every time you use a digital wallet or card, the software rounds the purchase to the nearest dollar and invests the change. While these amounts seem negligible, the cumulative effect over a fiscal year creates a substantial capital cushion. It's a method that prioritizes consistency over intensity, ensuring that every dollar spent contributes to your total net worth without requiring active management.

Behavioral Finance: Mastering the Psychology of Retention

To effectively learn savings, you must first master the cognitive biases that dictate your financial behavior. The most common barrier is the perception that you lack the capital to begin. Data from the 2024 Federal Reserve report indicates that 37% of adults couldn't cover a $400 emergency expense with cash. This often stems from a psychological block rather than purely insufficient income. Habitual retention starts with as little as 1% of your monthly earnings. This builds the neural pathways required for long-term wealth accumulation before you ever see a substantial pay increase.

Spending triggers the brain's reward system. Each click on an instant delivery app releases dopamine, which provides a temporary chemical high. This surge often masks the long-term erosion of your net worth. True financial mastery involves shifting that reward response from the act of consumption to the act of accumulation. You're training your brain to find satisfaction in the growing balance of a brokerage account rather than the arrival of a cardboard box. This shift requires a disciplined framework for delayed gratification that counters the "buy now" culture of 2026.

Combatting Lifestyle Inflation

Lifestyle creep occurs when your expenses rise in direct proportion to your income gains. High-earners frequently fail to build wealth because they lack rigid behavioral standards. They often equate professional success with external status markers, which leads to a cycle of high-burn spending. To disrupt this cycle, you should implement the "Wait 48 Hours" rule for any non-essential purchase exceeding $100. This cooling-off period allows your prefrontal cortex to override the initial emotional impulse. Decoupling your self-worth from material acquisition is a technical requirement for anyone who wants to learn savings at an elite level.

Setting High-Stakes Savings Goals

Vague intentions result in mediocre outcomes. You must transition to S.M.A.R.T. objectives. These are Specific, Measurable, Achievable, Relevant, and Time-bound. Research suggests that naming your savings accounts increases the likelihood of reaching your goal by 31%. Labeling a sub-account as a "Freedom Fund" or "Legacy Trust" creates an emotional barrier against impulsive withdrawals. It transforms a generic number into a tangible future asset that you're less likely to compromise for short-term desires.

- Specific: Define exactly what you're saving for, such as a six-month emergency fund.

- Measurable: Use automated tracking to monitor progress every 30 days.

- Time-bound: Set a hard deadline for the end of the fiscal year.

You can accelerate this transition by utilizing the best personal finance courses for beginners to formalize your strategy. These programs provide the structured environment needed to rewire your financial mindset for the current economic climate. By establishing these behavioral standards now, you ensure that your future income increases lead to wealth, not just higher bills.

Take control of your financial future by exploring the top-rated financial literacy modules available through IAB Academy.

From Saving to Investing: Scaling Your Wealth with IAB Academy

The transition from a "Savings Engine" to an "Investment Engine" is the most critical pivot in your financial lifecycle. While you learn savings strategies to protect your capital, investing is the mechanism that multiplies it. This shift shouldn't be governed by emotion or market hype; it must be a calculated move based on the stability of your retained capital. Mastery over your cash flow is the prerequisite for entering the global market ecosystem.

The Threshold of Investment Readiness

Your readiness to invest is defined by your risk tolerance and your liquidity. IAB Academy advocates for the "Six-Month Rule," a standard requiring 180 days of total living expenses to be held in a liquid, low-risk account before you allocate capital to volatile assets. This safety net ensures that a 15% market correction doesn't force you into a predatory liquidation of your portfolio. Without this foundation, market participation is merely gambling with your survival fund.

Professional wealth building requires a systematic approach to risk management. You should evaluate your readiness through these metrics:

- Debt-to-Income Ratio: Ensure high-interest liabilities are eliminated before seeking market returns.

- Capital Retention: Maintain a consistent 20% savings rate for three consecutive quarters.

- Educational Allocation: Use a portion of your saved capital to fund a personal finance class to ensure you understand the instruments you're buying.

Your Future with IAB Academy

The IAB Academy Novice Investor Curriculum is designed to bridge the gap between basic capital retention and sophisticated wealth generation. It's not enough to simply accumulate cash; you must understand how to deploy it. Our platform utilizes the Smart Instructor™, a real-time AI tutoring system that provides instant feedback as you analyze market trends and asset classes. This technology removes the intimidation factor from the stock market by providing data-driven insights tailored to your specific learning pace.

Whether you're starting with the IAB Teen Academy or moving directly into our advanced Novice modules, the path to mastery is disciplined and modular. You'll progress from understanding simple interest to mastering AI-powered stock analysis and programmatic portfolio rebalancing. This isn't just about picking stocks; it's about future-proofing your financial identity in a competitive global economy. Secure your lifetime access to our ecosystem today. Start building the mastery required to turn your savings into a legacy of wealth.

Mastering Your Financial Architecture for 2026

Implementing a structured 5-step system for capital engineering transforms abstract goals into a concrete financial foundation. By 2026, the global digital ecosystem demands a sophisticated approach to asset retention that utilizes automated technology and behavioral discipline. You've identified how to transition from basic retention to strategic wealth scaling; this shift is essential for professional advancement. It's time to learn savings through a lens of professional excellence. Success in this competitive landscape depends on your ability to apply these industry standards immediately.

The IAB Academy provides the definitive framework for this professional evolution. Our curriculum features an AI-Powered Smart Instructor™ available 24/7 to facilitate your mastery. Students receive lifetime access to all 2026 curriculum updates, ensuring your strategy remains compliant with emerging market standards. With specialized tracks designed for Teens and Novices, you'll establish the credibility required for long-term fiscal success. Master your financial future with IAB Academy's Novice Investor Curriculum. You have the tools to define your own economic trajectory.

Frequently Asked Questions

What is the best way to start learning savings for a complete beginner?

To effectively learn savings as a beginner, you must first establish a rigorous tracking system for every dollar of inflow and outflow. This foundational step provides the data necessary to identify inefficiencies in your spending patterns. According to a 2023 Federal Reserve report, 37% of adults lack the liquidity to cover a $400 emergency. You'll bridge this gap by automating a $50 monthly transfer to a separate account immediately to build initial momentum.

How much of my income should I realistically save in 2026?

You should aim to allocate 20% of your net income toward savings and debt reduction throughout 2026. This benchmark follows the 50/30/20 framework, where 50% goes to needs and 30% to wants. With 2026 inflation rates projected at 3.2% by economic analysts, maintaining this 20% threshold is vital for preserving purchasing power. It's a non-negotiable standard for anyone seeking long-term financial stability and professional growth in a competitive market.

Is it better to pay off debt or save money first?

You must prioritize paying off any debt with an interest rate exceeding 7% before building a large savings pool. Credit card interest rates reached an average of 22.8% in 2024, which far outpaces the returns in most standard savings vehicles. Secure a $1,000 starter emergency fund first; then direct all surplus capital toward high-interest balances. This strategic sequence prevents interest from eroding your net worth and ensures your financial foundation remains secure.

What is a high-yield savings account (HYSA) and do I need one?

A high-yield savings account is a federally insured deposit account that offers interest rates significantly higher than the national average. While traditional accounts often yield a mere 0.46%, top-tier HYSAs in 2025 provided rates above 4.5%. You need one to ensure your dormant cash maintains its value against inflation. It's an essential tool for your learn savings journey because it compounds your capital with zero risk and provides maximum liquidity for your assets.

Can AI really help me save money automatically?

AI-driven financial tools use predictive algorithms to analyze your cash flow and execute micro-transfers to your savings. These systems identify "safe to save" amounts, often as small as $2 or $5, without triggering an account overdraft. Industry reports indicate that 60% of Gen Z consumers now utilize fintech automation to build wealth. Implementing these tools removes the psychological friction of manual transfers and ensures consistent progress toward your mastery of modern financial management.

How do I save money if I am living paycheck to paycheck?

You can begin saving by implementing the "Pay Yourself First" protocol, even if you start with only $5 per week. A 2023 survey found that 63% of Americans live paycheck to paycheck, yet many can find small efficiencies by auditing recurring subscriptions. Treat your savings as a mandatory bill that you pay before any other expense. This shift in priority builds the discipline required for higher-level financial mastery and long-term career survival.

What is the difference between saving and investing?

Saving is the act of setting aside liquid cash for short-term needs, while investing involves purchasing assets to generate long-term wealth. Savings accounts provide immediate access and safety but lower returns. In contrast, the S&P 500 has delivered a 10% average annual return over the last 30 years, though it carries market risk. You must master the art of saving before you transition into the complexities of the stock market to ensure stability.

How many months of expenses should be in an emergency fund?

Your emergency fund should contain a minimum of 3 to 6 months of essential living expenses. This includes housing, utilities, food, and insurance premiums. If your monthly essentials total $3,000, your target reserve is between $9,000 and $18,000. This liquidity acts as a buffer against job loss or medical emergencies. It's the definitive standard for achieving professional financial security and peace of mind in a volatile global ecosystem.